24 What are instalment payments and how are they calculated for an individual?

Jeewanpreet Kaur

Instalment payments represent ongoing tax payments to the government throughout the year. They are usually required if an individual’s ‘net tax owing’ was greater than $3,000 (known as the ‘instalment threshold’) in either of the previous two taxation years. Typically this would occur when regular tax withholding payments throughout the year were insufficient (See ITA 156.1(2) for further details).

If an individual is required to make instalments, the payments will be made quarterly on March 15th, June 15th, September 15th and December 15th. As per ITA 156(1) Individuals (other than farmers and fishermen) can calculate their instalment payments using any of the following three methods:

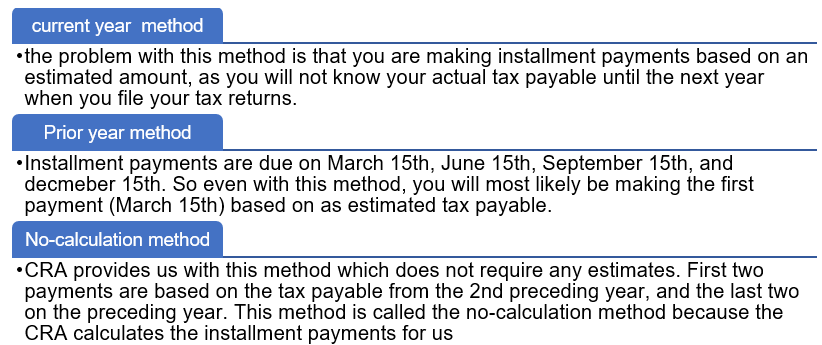

1) Current year option: The quarterly installments are based on the individual’s current year estimated tax payable.

2) Prior year option: The quarterly installments are based on the individual’s tax payable for the previous year (i.e. you would base your 2019 installments on your tax payable in 2018)

3) No-calculation option: The first two quarterly instalments are based on the tax paid in the second preceding taxation year (2017 is the second preceding year for 2019) and last two instalment payments are based on the tax paid in the preceding taxation year. This calculation is explained in more detail below.

Why are there three options available? Largely this has to do with the problems in guessing or estimating the instalment amounts using the current year or prior year methods.

The individual can choose any of the available options according to his/her discretion. Typically the taxpayer would choose the option with the least tax paid up front.

Under the ‘no-calculation’ method the instalments are determined as follows (for 2019):

- (a) an amount equivalent to 1/4 of the installment base of the second preceding taxation year (2017) is to be paid on March 15, 2019 and June 15, 2019. And

- (b) for the installments to be paid on September 15, 2019 and December 15, 2019, the amounts already paid under (a) are deducted from the total tax paid in the preceding taxation year (2018). The resulting amount is then spread over the last two installments.

For example, John’s estimated tax payable for 2019 is $16,881. He paid $11,250 for 2018 and $9,750 for 2017 as tax. The calculation for tax installments payable under three available options for 2019 is as follows:

|

Payment Date |

Current year Option |

Prior Year Option |

No-calculation Option |

|

|

Estimated Tax Payable for 2019 = $ 16,881 |

Tax Paid for 2018=$11,250 |

Tax Paid for 2017=$9,750 Tax Paid for 2018=$11,250 |

|

March 15, 2019 |

(16881/4) = $4,220 |

(11250/4) $2,813 |

(9,750/4) $2,438 |

|

June 15, 2019 |

$4,220 |

$2,813 |

(9,750/4) $2,438 |

|

September 15, 2019 |

$4,220 |

$2,813 |

(11,250-2,438-2,438)/2 $3,187 |

|

December 15, 2019 |

$4,221 |

$2,811 |

$3,187 |

|

Total |

$16,881 |

$11,250 |

$11,250 |

Note, under option #2 and option #3 John would need to make a final payment of $5,631 on April 30th, 2020 to get the total payments for the year to equal his overall tax liability (assuming he ultimately owed $16,881 for the year).

Interactive content (Author: Jeewanpreet Kaur, March 2019)

Interactive content (Author: Sambhav Chaudhary, March 2019)

References and Resources:

- ITA 156(1)

- Competency map: 6.4.1

March 2019

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the authors of the text.

Image Description

Figure 24.1 Image Description: There are three methods of calculating installation payments. For the current year method all payments are based on estimates. Prior year method the first payment is based on estimates. Lastly, no calculation method does not rely on any estimates. [Return to Figure 24.1]