37 What are the key rules related to an RESP?

H. Khosa

A Registered Education Savings Plan (RESP) is a contract between the Subscriber and the Promoter for the Beneficiary to have a chance at attaining higher education. The Subscriber is the person who set up the RESP and is usually the primary caregiver (often the parent) of the Beneficiary. The Beneficiary is the child who will use the RESP for education costs.

There are two types of promoters for RESP’s: financial institutions (ex. RBC or Credit unions) and group scholarship providers (ex. Canadian Scholarship Foundation). The Promoter is the one who organizes all the detail and manages the RESP. They are also the ones who pay the contributions to the Beneficiary. The Beneficiary must be a resident of Canada. Unlike an RRSP, Subscribers cannot deduct the contributions to an RESP from their income on their income tax return.

How do you contribute to an RESP?

It depends on your RESP promoter. For example, you may have entered a plan where your provider requires a certain amount of contributions monthly or annually each year. Others let the Subscriber contribute to the plan whenever the Subscriber wants. As of 2019 the maximum amount for a Subscriber to contribute to an individual’s RESP is $50,000 during their lifetime.

There is also a federal government grant that is called the Canada Education Savings Grant (CESG). As of 2019, the maximum lifetime amount that the CESG can provide is $7,200. The CESG is 20% on the first $2,500 or less per year of contributions made by the Subscriber to an RESP. There are additional CESG amounts available to help out lower income families as follows:

“10% on the first $500 of annual personal contributions for children from families with an adjusted family net income between $46,605 and $93,208.” (CRA)

“20% on the first $500 of yearly personal contributions for children from families with an adjusted family net income of $46,605 or less.” (CRA)

How do you optimally withdraw $ from an RESP?

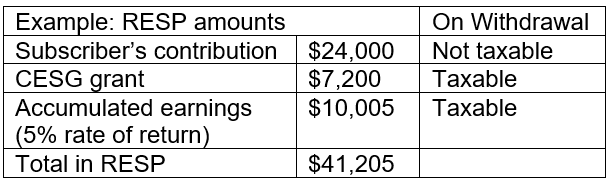

The best way to withdraw money from an RESP is by having the Beneficiary pursue post-secondary education. The Subscriber’s contribution, the CESG, and accumulated earnings are paid out to the Beneficiary as Educational Assistance Payments (EAP). The Subscriber’s contribution is not taxable to the Beneficiary or Subscriber, but the CESG and accumulated earnings are taxable income to the Beneficiary.

If the Beneficiary does not use the RESP, the Subscriber has a few options. Firstly, the RESP can be transferred to another Beneficiary, or the RESP can be refunded. The original Subscriber contribution can be returned to the Subscriber tax-free. For the accumulated earnings it depends on what kind of plan the Subscriber has. Some plans forfeit the earning or they can be paid out as Accumulated Income Payments (AIP) to the Subscriber. AIP is subject to regular income tax plus an additional 20% tax, or 12% for residents of Quebec. In general it is much better to have the Beneficiary withdraw amounts while they are attending school because usually, the Beneficiary’s income level is low at that time.

Interactive content (Author: H Khosa, March 2019)

Interactive content (Author: Saijal Arora, June 2019)

References and Resources:

- ITA – 146.1(1)

- Article-“Registered Education Savings Plans”(Author: Government of Canada)

- Article-“What is a Registered Education Savings Plans (RESPs)?”(Author:TaxTips.ca)

- Competency map: 6.3.3

January 2019

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.