54 What are Other Incomes and Other Deductions?

Jaydeep Shergill

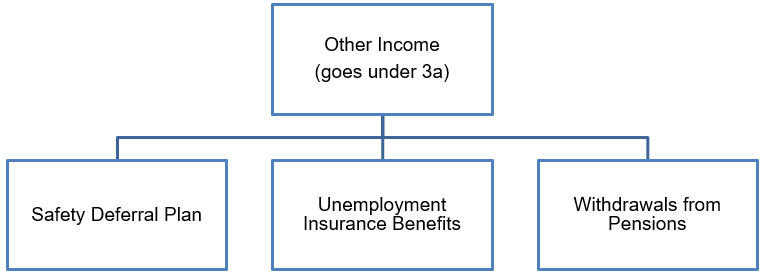

According to ITA 56(1), other income amounts to be included in the recording of income tax are amounts not obtained through employment, business, or property income such as: pension benefits (CPP, provincial pension plans, and private pension benefits), unemployment insurance benefits, parts of registered pension plans that are redeemed within a tax year, spousal support payments received, and salary deferral plans.

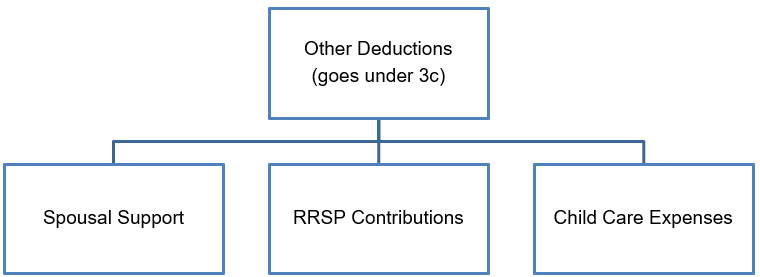

Other Deductions are similar to other income in that they do not originate from employment, business, or property income. ITA 60 states, “There may be deducted in computing a taxpayer’s income for a taxation year such of the following amounts as are applicable: Support payments made, Pension income reallocation, Repayment of support payments…”. Examples of these “Other Deductions” include childcare expenses, spousal support payments paid, moving expenses, and deducted RRSP contributions.

It is important to identify whether certain items represent income or a deduction. For example, spousal support payments received would be included as income in 3(a) whereas spousal support payments made would be deductible in 3(c).

Order of Other Income and Other Deductions in Calculating Net Income for Tax Purposes:

Other Income amounts are included under ITA 3(a) in the calculation of Net Income for Tax Purposes. Other deductions are applied against the sum of ITA 3(a) and ITA 3(b). If the 3(c) exceeds the sum of 3(a) and 3(b) then the subtotal is $Nil. Although there are some exceptions most of the ITA 3(c) deductions are “use it or lose it” deductions meaning that they expire if they are not used within the year.

Interactive content (Author: Jaydeep Shergill, January 2019

References and Resources:

- ITA 56, ITA 56(1), ITA 60, ITA 248(1)

- Competency map: 6.3.2

January 2019

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the authors of the text.