13 What options are available when a taxpayer disagrees with a CRA assessment?

Karen Rana

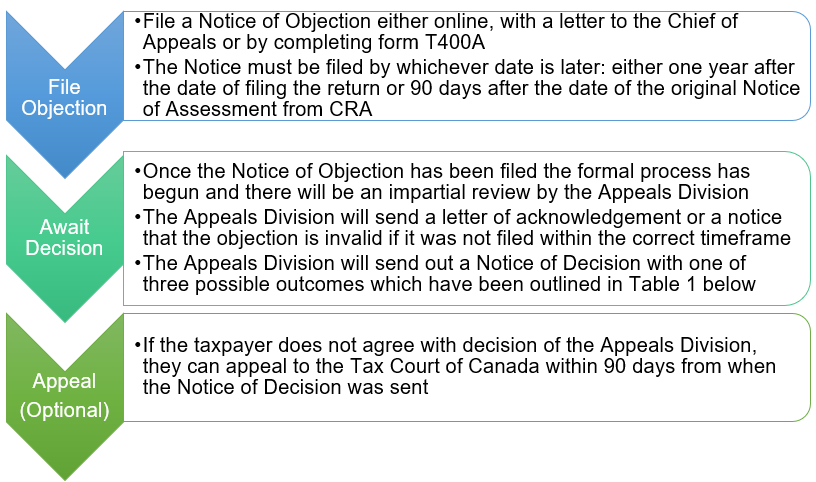

If a taxpayer receives their CRA assessment and disagrees with it, they have the option to dispute it. Before filing an official objection, taxpayers are encouraged to contact their local CRA tax office to resolve their issue. If that does not address their concern, the next step is to file a Notice of Objection and the process of doing so has been outlined below.Ed Note: In the “File Objection” section below it should say “either one year after the filing due date or 90 days…” rather than “either one year after the date of filing the return or 90 days”

As mentioned above, there are three possible decisions that the Appeals Division can make. The three outcomes have been listed in further detail below.

|

Decision |

Action |

Reasoning |

|

The objection has been allowed in full |

The assessment under question is fully reversed as the Appeals Division agrees with the taxpayer; the amount due on the assessment is reversed |

Additional information was made available to the CRA which changed the circumstances |

|

The objection has been partly allowed |

The Appeals Division agrees with parts of the objection but not all of it so the amount due is adjusted based on what the Appeals Division agrees with. A reassessment will be issued to reflect the adjustment. |

It is decided that the taxpayer is correct on some of the objections raised. |

|

The objection has been denied |

The Appeals Division does not agree with the taxpayer; the amount due is upheld and the taxpayer must pay the full amount due plus interest |

The taxpayer cannot demonstrate that the original assessment was incorrect and therefore nothing is changed |

For more information regarding this topic, please refer to Section 165(1) of the Income Tax Act which briefly outlines the process of filing an objection or the article linked below.

Interactive content (Author: Karen Rana, March 2019)

Interactive content (Author: Caitlin Lum, June 2019)

References and Resources:

- Article – “Guide to Objecting to a CRA Assessment” (Author: Tax Solutions Canada)

- Article – “File an appeal to the Court – Income tax or GST/HST” (Author: Government of Canada)

- Competency map: 6.1.1

March 2019

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.