44 What are taxable capital gains and allowable capital losses?

Jasmine Marahar

Capital Gains are the profits realized from the sale of Capital Property (see ITA 54 for definition). Although the arguments over whether transactions create business income, property income or capital gains can become pretty complex, in general, if the sale of an asset is a bi-product of its main purpose then it likely creates a capital gain (loss).

A standard example is an apple tree in an orchard business that sells apples. Typically the ongoing sale of apples would generate business income while the sale of the actual apple tree would create a capital gain.

Only 50% of a Capital Gain is included in income, this is known as the Taxable Capital Gains (“TCG”). For example, if the Capital Gain is $30,000, then the TCG would be $15,000 ($30,000 x 50%). Similarly, Allowable Capital Losses (“ACL”) are equal to 50% of the Capital Loss [ITA 38(b)]. ACL’s are deducted against TCG’s in the year.

Where do TCG’s and ACL’s go in the S3 ordering rules? What happens if your ACL > TCG?

In terms of the S3 ordering rules, capital gains and losses recorded in Net Income for Tax Purposes in 3(b). ACL’s are netted against TCG’s however the amount in section 3(b) cannot be negative. If ACL’s are greater than TCG’s then 3(b) will be $Nil and the difference becomes a Net Capital Loss that can be applied against net TCG’s in other years.

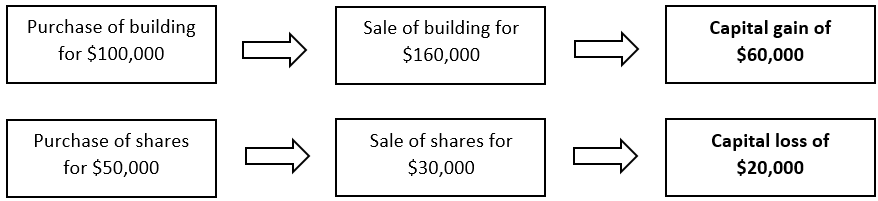

Example: Kylee sold two of her properties last year, a building and some shares, both purchased in 2016. There was no depreciation on the building. The building was bought at a price of $100,000, and sold for $160,000. The shares were bought at $50,000 and sold for $30,000.

The first transaction realized a capital gain of $60,000 and the second transaction realized a loss of $20,000. Kylee’s TCG would be ($60,000 x 50%) $30,000 and her ACL would be ($20,000 x 50%) $10,000. The amount recorded in 3(b) would be $20,000 (TCG-ACL).

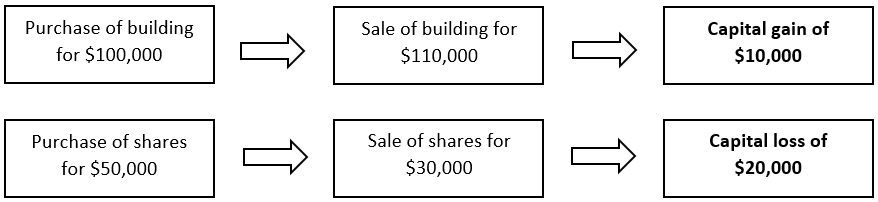

Now, let’s say Kylee bought the building for $100,000, and sold it for $110,000. The shares she bought for $50,000 and sold for $30,000.

The first transaction realized a capital gain of $10,000, and the second transaction realized a capital loss of $20,000. Kylee’s TCG would be ($10,000 x 50%) $5,000. Her ACL would be ($20,000 x 50%) $10,000. ACL>TCG, therefore the amount recorded in 3(b) would be $Nil and the $5,000 difference ($10,000-$5,000) would be added to her Net Capital Loss balance and could be applied against 3b amounts in other years.

Interactive content (Author: Karn Thiara, June 2019)

Interactive content (Author: Afeef Khan, July 2019)

References and Resources:

- ITA 248(1) “capital gain”, “property”, ITA 38(b),

- Article – “Capital Gains and Losses.” (Author: TaxTips)

- Competency map: 6.3.2

January 2019

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.