60 Child Care expenses and how they are treated for tax purposes?

Bhavish Toor

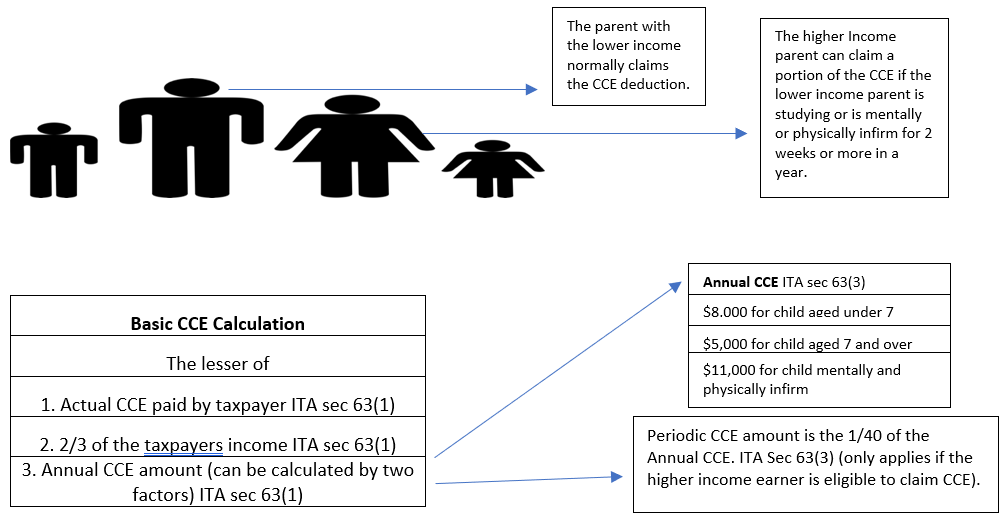

Child care expenses are amounts you or your spouse or Common-law partner spend to have someone look after an eligible child so that you or the other person could work to generate income or handle business or attend school ITA 63 (3). An eligible child is

- Under the age of 16 at any time during the year (exceptions are made to the age limit if the child is mentally or physically infirm).

- You or your spouse’s or common-law partner’s child.

- Was dependent on you, your spouse or common-law partner in the taxation year.

Examples of child care expenses (“CCE”) are the amount paid to a child care provider, day care centers, day nursery school, nannies, day camps and overnight camps, not including fees paid for education, leisure or recreational activities, medical or hospital bills, clothing or transportation cost.

CCE is recorded as deductions in section 3(c) of the section 3 ordering rules, when calculating Net Income for Tax Purposes.

Who can claim the CCE?

Ed.Note: Per ITA 63(2), for the higher income spouse to claim some of the childcare expenses, the lower income spouse must be attending school for a minimum of 3 weeks or in a hospital or imprisoned for a minimum of 2 weeks.

In order to understand it in much detail there is a good example in income tax folio S-1,F-3,C-1 on paragraph 1.44.

Example: Martina and Joe sent their kids Max, age 19, with a disability; Jax, age 6; and Rex, age 4, to a summer camp for 4 weeks. The total cost for the camp was $4,500. They also incurred $11,090 in regular childcare during the year. Martina has earned income of $55,000 and Joe has earned income of $61,000.

Calculate the deductible childcare costs to see which would be the least of the 3 methods. (Actual, 2/3, Annual)

ITA 63(3) Annual Child Care Expense Amount

Max 19 with a disability = $11,000

Jax 6 =$8,000

Rex 4 =$8,000

To get the weekly eligible amount (Actual Amount) we divide the Annual Expense Amount by 40 to get the following:

Max 19 with a disability = $11,000 divided by 40 = $275

Jax 6 =$8,000 divided by 40 = $200

Rex 4 =$8,000 divided by 40 = $200

Martina is the lower income spouse and, since the exceptions in 63(2) don’t apply, she will be the one claiming the childcare expenses for the year. Here is the calculation.

2/3 method = $55,000 x 2/3 =$36,667

Annual Method =$8,000 + $8000 + $11,000 =$27,000

Actual Method = $11,090 + (($200 + $200 + $275) X 4 weeks) =$13,790

Since Martina is the Lower Income Spouse, her deduction will be $13,790 (the lesser of the three amounts calculated above)

(Example by: Priya Dhariwal)

nteractive content (Author: Bhavish Toor, March 2019)

Interactive content (Author: Arminder Sandhu, June 2019)

References and Resources:

- ITA 63; 63(2), 63(3)

- Article – “Income Tax Folio S-1, F-3, C-1, Child Care Expense Deduction”, (Author- Government of Canada)

- Image – “family” by Bhavish Toor licensed under CC BY 4.0

- Competency map: 6.3.2

January 2019

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.

{kind=link}