3 Describe Qualitative Characteristics of Taxes. Provide some examples of each in Canada.

Cynara Almendarez and Marc Kampschuur

Qualitative Characteristics

The definition of “fairness” may depend on an individual’s point of view. If a person earns double the income, should the person pay:

- double the income tax as a consistent ratio is `fair’;

- more than double the income tax as with greater ability to pay this is ‘fair’ (progressive tax); or,

- less than double the income tax as the taxpayer’s consumption of public services is unlikely to be double thus this is `fair’ (regressive tax)?

Hence when we discuss the the `fairness’ of a tax we often reference specific qualitative criteria such as presented in this activity:

Note that it may be `fair’ to stimulate investment in a sector (e.g. recycling…) or savings for retirement which in terms of qualitative characteristics would not be `neutral’

Regressive taxes are applied uniformly, and they do not change based on an individual’s level of income. A regressive tax system affects low-income taxpayers more than high-income taxpayers because it takes a higher percentage of their earnings.

A great example of a regressive tax is the 5% Goods and Services Tax (GST). For example, say a doctor earns $175,000 annually and a retail worker earns $30,000 annually. They both purchase a laptop for $1,000, and are charged $50 GST ($1,000 X 5%). Although the $50 GST amount is the same for both the doctor and the retail worker it is a higher percentage of the retail workers overall income. This is known as a regressive tax because it has a larger percentage impact on lower income individuals.

![The GST for the retail worker's income is calculated as [($50/$30,000) x 100]](https://kpu.pressbooks.pub/app/uploads/sites/217/2019/04/2019-03-14-7-1-300x135.png)

![The GST for the doctor's income is calculated as [($50/$175,000) x 100]](https://kpu.pressbooks.pub/app/uploads/sites/217/2020/12/2019-03-14-7-300x143.png)

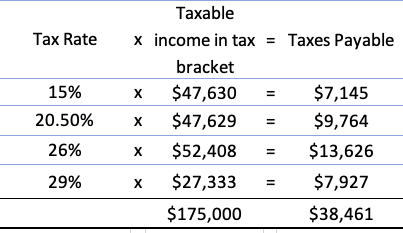

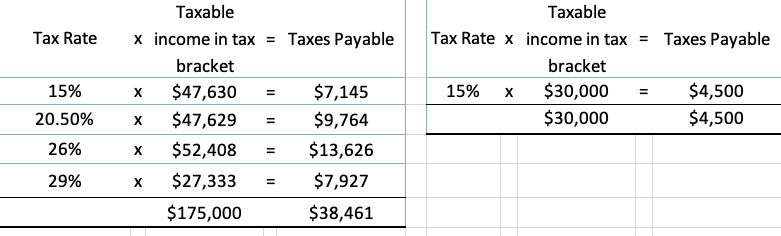

Progressive taxes are the opposite of regressive taxes. Progressive taxes increase based on your taxable income. Canada has a progressive income tax system; therefore, high-income taxpayers pay a progressively higher percentage of tax than low-income taxpayers. Using our previous example, because of the doctor’s higher annual income, the doctor will have to pay more taxes than the retail worker based on Canada’s federal tax rates of 2018.

The doctor will have to pay $38,461 in taxes (an average tax rate of 21.98%) while the retail worker will only have to pay $4,500 of taxes (an average tax rate of 15%). Progressive taxes get progressively higher as your taxable income increases.

Doctor Teacher

Interactive Content (Author: Cynara Almendarez, January 2019).

Interactive Content (Author: Joyce Hards, April 2019)

Interactive content (Author: Matthew Amisano, January 2020)

References and Resources:

- Article – “Canadian Income Tax Rates for Individuals – Current and Previous Years” (Author: Government of Canada)

- Article – “Tax battle with paper company won by B.C. town” (Author: CBC).

- Article – “Catalyst Paper, City of Powell River achieve unique tax solution” (Author: Catalyst).

- Competency map: 6.1.1

January 2020

Media not mentioned below is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) and owned by the author of the text.