11 What is the Alternative Minimum Tax? How is the AMT applied? Why does it exist?

Sharon Basi and Marc Kampschuur

What is the Alternative Minimum Tax?

The Alternative Minimum Tax has been in effect since 1986. “It is a means to bring fairness to the tax system.” (RBC Wealth Management, p.1). The AMT prevents the wealthy and middle class high-income earners and trusts from using certain tax incentives to reduce or eliminate their tax obligations.

How is AMT applied?

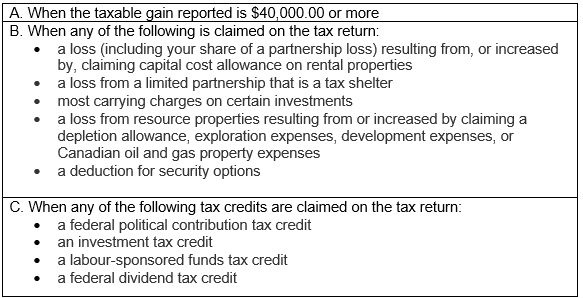

AMT is usually triggered when high-income earners invest in tax shelters (uch as limited partnership units) or earn income from sources that receive preferential tax treatment that may be disproportionately available to high income earners (such as dividends and capital gains). AMT only applies to individuals and trusts and not to corporations. According to the CRA the following table is a list of some of the most common situations in which people need to pay the minimum tax. Note that the amount by which AMT exceeds regular tax is refundable within the seven years after it was paid by the amount regular tax exceeds AMT.

Information Retrieved from CRA webpage

The calculation of the Alternative Minimum Tax can be found in 127.51 of the ITA

Why does it exist?

AMT exists because the government wants those who earn higher incomes to pay at least a minimum amount of tax rather than paying less tax than the lower income earners or even no tax, due to having more incentives than those who earn less.

Interactive content (Author: Sharon Basi)

References and Resources:

- ITA- 12.7.5-127.55

- Article – “Minimum Tax” (Author: Government of Canada)

Jan 2021

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.