2 Who is liable to pay tax in Canada and on what sources of income?

Sam Newton and Marc Kampschuur

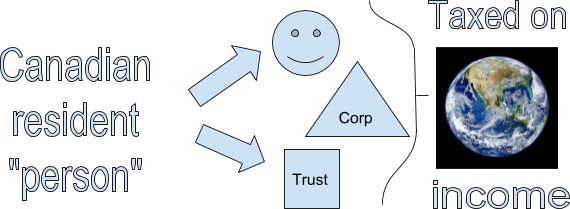

Basically, every person resident in Canada is required to pay income tax on their worldwide taxable income. A “Person” is defined in the Income Tax Act (“ITA”) as a corporation, individual or a trust. Accordingly, there are three taxable entities in our Income Tax System. Relevant sections from the ITA include:

ITA S.2(1) which states that “An income tax shall be paid, as required by this Act, on the taxable income for each taxation year of every person resident in Canada at any time in the year.”

ITA S.248(1) which defines a “Person” as a corporation, individual or trust and ITA 3(a) states that a taxpayer’s income includes sources “inside or outside Canada”. Therefore, Canadian resident corporations, individuals and trusts are taxed on their worldwide income

“Persons” non-resident in Canada are required to pay tax on their Canadian source income, which is basically income earned/generated in Canada (See ITA S.2(3) for further details).

Why are residents taxed on worldwide income and non-residents taxed only on Canadian sourced income?

Residents are taxed on worldwide income to discourage individuals and corporations from storing their assets and sourcing revenue in tax havens with low tax rates (like Switzerland or the Cayman Islands) to avoid tax. Since Canadian residents are taxed on worldwide income there may be no point in sourcing your income in a low tax country if you – as a resident of Canada – are still required to pay tax on the income in Canada.

Non-residents are only taxed on their Canadian source income, and disposition of taxable Canadian property, as it wouldn’t seem fair to tax someone on their worldwide income if they aren’t resident in Canada. For example, let’s say a software developer resident in Mexico temporarily moves to Canada for 2 months and takes a contract with Hootsuite. Although she would be taxed in Canada on her income earned in Canada for the 2 months, it wouldn’t make sense (or be fair) to tax her in Canada on her income earned in Mexico during the rest of the year. Taxable Canadian property includes real property, business property, and shares in Canadian corporations. Thus if the software developer purchased real estate in Canada while on contract then tax is payable when this property is sold irrespective that resident in Mexico at the time of the sale.

Interactive content (Author: Kokila Sharma, June 2019)

References and Resources:

- ITA – 2(1), 2(3), 3(a), 248(1) “Persons”

- Competency map: 6.1.1

January 2020