54 How do the various corporate tax rates tie into the concept of integration?

Chanpreet Kang

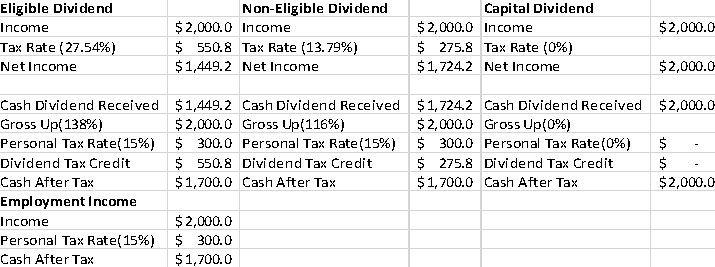

The idea behind integration is that regardless of how you earn your income (through a corporation or directly) the ultimate amount of after tax cash should be the same. This should be true regardless of whether a corporation earns active or passive income or pays out eligible, non-eligible or capital dividends. This is illustrated below:

Note: There is a minor mathematical issue in the non-eligible dividend portion of the table above. The corporate tax rate should be slightly lower, the gross up should be 115% rather than 116% and the dividend tax credit would be slightly lower.

This figure shows that you end up with the same amount of after tax cash (for a given income type) regardless of whether it was earned directly or received through corporate dividends. This applies to capital dividends as well as they are flowed through tax free to the shareholder (to represent the tax free portion of capital gains).

Passive or aggregate investment income is taxed very differently compared to the other forms of income. It is taxed at a very high rate and a large amount of this tax goes into the non-eligible RDTOH account. Ultimately this amount is refunded to the corporation when they subsequently pay out non-eligible dividends. The tax rate on aggregate investment income less the dividend refund (when dividends are subsequently paid out) bring the net amount of tax paid on AII to an amount similar to Active Business Income eligible for the Small Business Deduction. For this reason, AII creates non-eligible dividends even though it is initially taxed at a very high rate.

Interactive content (Author: Alicia Mitchell, January 2020)

References and Resources:

- Article – taxable amount of dividends (eligible and other than eligible) from taxable Canadian corporations, (Author: Government of Canada)

- Article – Income Tax Folio S3-F2-C1, Capital Dividends, (Author: Government of Canada)

- Article – Federal Dividend Tax Credit, (Author: Government of Canada)

- Article – T2 Corporation – Income Tax Guide – Chapter 7: Page 8 of the T2 return (Author: Government of Canada)

January 2020

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.