22 What is a non-arm’s length transaction and what are the tax implications?

Vianna Tran

CRA defines a non-arm’s length transaction as “a relationship or transaction between persons who are related to each other.”

ITA 251(2)(a) describes related persons as “individuals connected by blood relationship, marriage or common-law partners or adoption” with 251(6) elaborating on what is meant by “blood relationship”.

Why is the government concerned about non-arm’s length transactions?

ITA 248(36) states that fair market value should be applied to the transaction of the property. However, in a non-arm’s length transaction it is not always relied on that fair market value was used. In a related party transaction the related individuals may be able to work together to set the property below or above fair market value to their tax advantage.

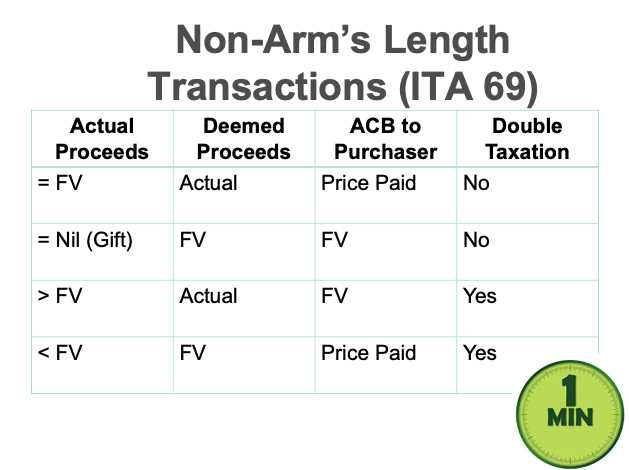

ITA 69(1)(a) describes inadequate considerations as “where a taxpayer has acquired anything from a person with whom the taxpayer was not dealing at arm’s length at an amount in excess of the fair market value thereof at the time the taxpayer so acquired it, the taxpayer shall be deemed to have acquired it at that fair market value.” Effectively, the ITA 69 rules state that non-arm’s length transactions that are not recorded at fair value will result in extra taxation. For the seller they do this by recording the transaction at the greater of FMV and actual proceeds therefore maximizing the potential capital gain. For the purchaser they do this by recording the transaction at the lesser of FMV and actual proceeds thereby minimizing potential future CCA claims or maximizing capital gains on future sales of the asset.

You could be subject to double taxation if you are dealing in a non-arm’s length transaction, and the CRA thinks you may be selling (or buying) something for not the fair market value to gain some kind of advantage for tax purposes.

Example (Proceeds < Fair Market Value by Manmeet Kaur):

Assume Manmeet bought a rental property in 2019 for $500,000. Two years later, she sold it to her brother, Isaac for $600,000 even though the fair value was $800,000. They made the sale at the reduced price so that Manmeet could minimize her capital gain.

How does ‘extra’ taxation take place in this scenario and to what extent?

As per ITA 69, Manmeet is deemed to have sold the property at the $800K fair value (rather than the $600,000 selling price) which will result in a $300,000 capital gain. Her brother Isaac, however, will only be able to record the cost base at the actual selling price ($600,000) which will increase his capital gain (or reduce the amount of tax depreciation he can claim) if he were to sell it in the future.

Ultimately, Manmeet and her brother are double/extra taxed as they didn’t record their non-arm’s length transaction at fair value.

Interactive content (Author: Ishneet Sehgal, June 2019)

References and Resources:

- ITA – 69(1)(a), 251(2)(a), 248(36)

- Article – “Non-arm’s length transactions” (Author Government of Canada)

- Article – “Definitions for letter N (Business)” (Author: Government of Canada)

- Competency map: 6.3.2

January 2019

Media Attributions

- Non-Arm’s Length Transactions table © CPA Canada is licensed under a CC BY-NC-SA (Attribution NonCommercial ShareAlike) license