5 Explain the tax concept of “integration”

Eva Viernes

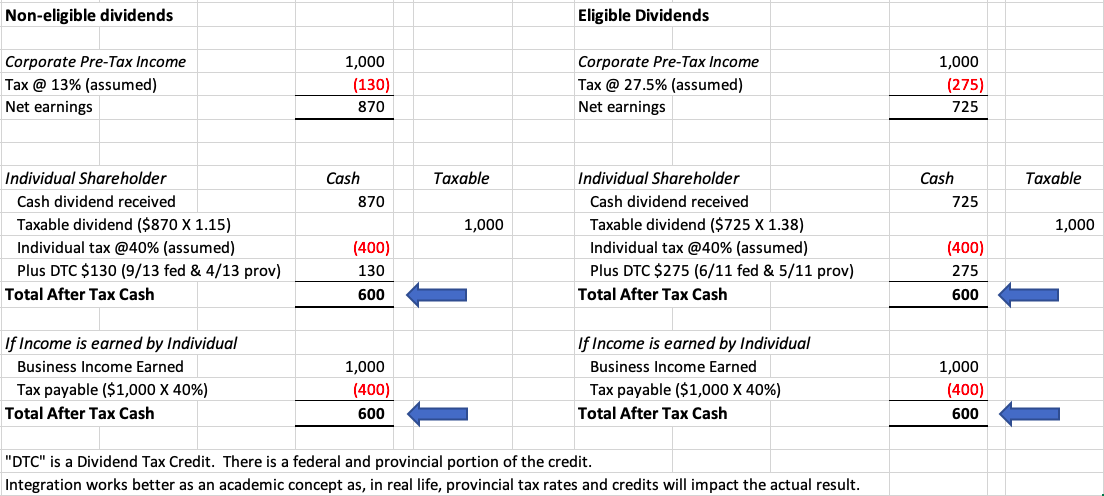

The concept of integration is intended to eliminate any advantages and disadvantages in the application of tax between individuals, corporations and trusts. Thus, the after-tax cash received by an individual should be the same regardless if it was generated directly (as salary) or paid out as dividends from a corporation.

To achieve integration and to avoid double taxation on dividends received from a corporation, an individual must:

• gross-up dividends received to reflect the corporate pre-tax income

• receive a dividend tax credit (DTC) for the tax deducted at the corporate level

The DTC is the sum of federal and provincial dividend tax credits, and the calculation varies depending on whether the corporation is issuing eligible or non-eligible dividends. Typically, public corporations issue eligible dividends while Canadian-Controlled Private Corporations (CCPCs) issue non-eligible dividends.

Eligible dividends are paid from income that is taxed at a higher corporate rate, while non-eligible dividends are paid from income that is taxed at a lower corporate rate. To offset this inequity (and to create integration) eligible dividends receive more favourable tax treatment than non-eligible dividends.

Here is an illustration showing how integration works for both types of dividends. Notice that the tax paid by the corporation is equal to the DTC that can be claimed by the individual shareholder. The computed tax payable amount and the total after tax cash is the same irrespective of whether it is paid through eligible dividends, non-eligible dividends or received directly as salary.

Interactive content (Author, Eva Viernes, March 2019)

Interactive content (Author: Pooja Devi, June 2019)

References and Resources:

- Video – “Integration” (authors: Abjeet Khatra and Gursimran Kohli) – uses 2017 rates

- Competency map: 6.1.1

Media Attributions

- Example © Sam Newton is licensed under a CC BY-NC-SA (Attribution NonCommercial ShareAlike) license