37 What are the specific rules on the disposition of land and building? Why are these rules created?

Bushra Manghat

When there is a disposition of real property, the allocation of the proceeds between land and building can have a significant impact on the sellers taxable income. A large amount allocated to the land will create or increase the capital gain, with only half of this amount being taxable. At the same time, by manipulating the proceeds and allocating a smaller amount to the building you could potentially end up with a large terminal loss, which is fully deductible. The ITA 13(21.1) rules are intended to patch this loophole.

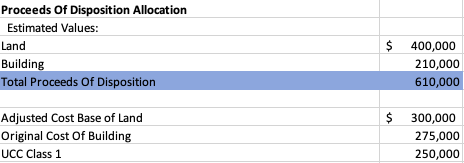

Example: Yasmeen Ltd. owns some land with a building on it. During 2018, the company sells the land and building for $610,000 and allocates the proceeds as follows:

As mentioned earlier, there is an incentive for Yasmeen Ltd. to allocate more of the proceeds to the land (creating a capital gain that is only 50% taxable) and to minimize the amount allocated to the building (to create a 100% deductible terminal loss)

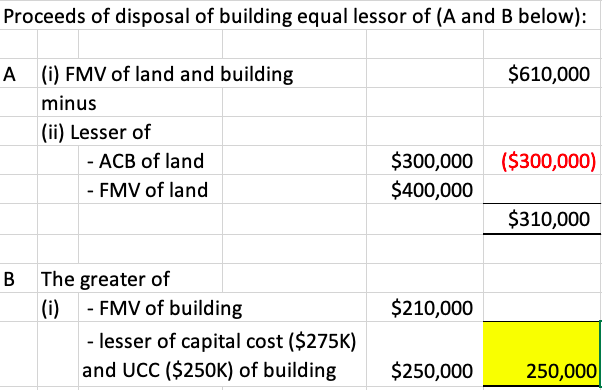

Being aware of this incentive, ITA 13 (21. 1) (a) contains a provision that can serve to limit the amount of any terminal loss that might arise on the disposition of real property. Applying this to the example this would require deemed proceeds of disposition for the building to be determined as the lesser of the two values:

By allocating $250,000 to the building you eliminate any terminal loss (as the $250,000 deemed proceeds equals the UCC). The remaining amount of the proceeds ($360,000) is then applied to the land which creates a smaller capital gain.

Interactive content (Author: Jason Gill, January 2020)

Interactive content (Author: Manpreet Singh, January 2020)

References and Resources:

- ITA 13 (21. 1) (a)

January 2020

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.

Image Description

Figure 38.1 Image Description: Total proceeds of disposition = $610,000 Adjusted cost base of land = $300,000 Original cost of building = $275,000 UCC class 1 = $250,000. [Return to Figure 38.1]

Figure 38.2 Image Description: Proceeds of disposal of building = (A) FMV of land and building minus lessor of ACB of land and FMV of Land. (B) the greater of FMV of building or lessor of capital cost and UCC of building. [Return to Figure 38.2]