36 What are ‘inducements’ and what are the tax implications?

Diane Macutay

Purpose of Inducements

Lease inducements, also known as tenant inducements, are used by landlords to attract tenants or to retain existing ones to their property. This usually occurs when there are more properties available than tenants in the market, and therefore landlords offer inducements in exchange for a signed lease. There are several different forms of inducements: non-cash inducements such as a lease buy-out, rent-free period or rent reduction, and cash inducements such as cash payments directly or for property improvements.

Tenant’s Perspective

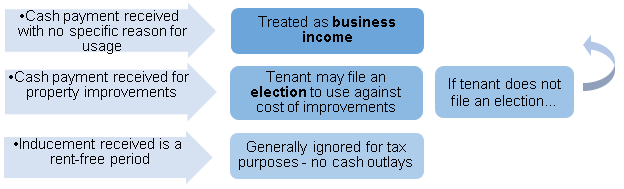

ITA s 12(1)(x) states that inducements are fully taxable at the time they were received. If a cash payment is received from the landlord solely as an exchange for a signed lease, the entire amount must be included in the tenant’s business income for that year.

However, if a cash payment is received for the purpose of improving the property, the tenant can file an election, as long as the original capital cost is greater than or equal to the inducement received. This allows the tenant to use the elected amount against the cost of the property improvement (Class 13 – leasehold improvements), eliminating the income inclusion. If the tenant does not file an election, the entire amount must be included in the tenant’s business income for the year.

Filing an Election to CRA

Since there is no specific form for filing an election, the taxpayer can simply prepare a letter attached to his or her income tax return. The election is due the same time the income tax return is due for that year. The letter must include the following:

- ITA section under which the election is made – s 13(7.4)

- Amount elected

- Amount of inducement and date received

- The date the property was acquired

- The original cost of the property (before reduction)

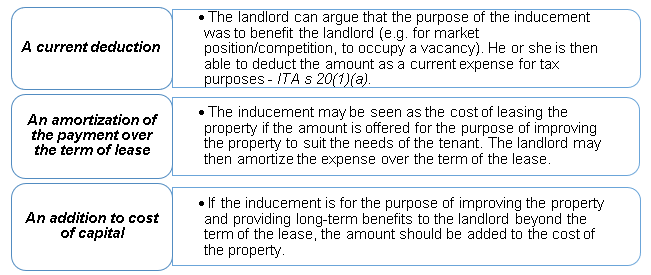

When landlords offer inducements, depending on the situation, these inducements can result in:

Interactive content (Author: Pooja Devi, January 2020)

Interactive content (Author: Harman Sandhu, January 2020)

References and Resources:

- ITA – 12(1)(x), 20(1)(a), 20(1)(hh), 53(2)(s)

- Article – “Canadian Income Tax Treatments of Leasehold Inducement Agreements” (author: Chris Munn)

- Article – “What is a Lease Inducement?” (author: Lillian Teague)

January 2020

All media in this topic is licensed under a CC BY-NC-SA(Attribution NonCommercial ShareAlike) license and owned by the author of the text.

Image Description

Figure 36.1 Image Description: Cash payments received with no specific reason treated as business income. Cash payment received for property improvements tenant may file an election to use against cost of improvements. Inducements received as a rent-free period are generally ignored for tax purposes. [Return to Figure 36.1]

Figure 36.2 Image Description: Landlord can argue the purpose of the inducement was to help the business. Thus, they can deduct the amount as a current expense. If the inducement is seen as the cost of leasing the property if the amount is offered for the purpose of improving the property. The landlord may then amortize the expense over the term. If the inducement is for the purpose of improving the property and providing long-term benefits, the cost should be added to the cost of property. [Return to Figure 36.2]