Motivating Employees Through Goal Setting and Incentives

3. 3 Motivating Employees Through Goal Setting

Goal-Setting Theory

Goal-setting theory (Locke & Latham, 1990) is one of the most influential and practical theories of motivation. In fact, in a survey of organizational behaviour scholars, it has been rated as the most important (out of 73 theories) (Miner, 2003). The theory has been supported in over 1,000 studies with employees ranging from blue-collar workers to research-and-development employees, and there is strong support that setting goals is related to performance improvements (Ivancevich & McMahon, 1982; Latham & Locke, 2006; Umstot, Bell, & Mitchell, 1976). According to one estimate, goal setting improves performance at least 10%–25% (Pritchard et al., 1988). Based on this evidence, thousands of companies around the world are using goal setting in some form, including Coca Cola Company, PricewaterhouseCoopers International Ltd, Nike Inc, Intel Corporation, and Microsoft Corporation, to name a few.

Setting SMART Goals

Are you motivated simply because you have set a goal? The mere presence of a goal does not motivate individuals. Think about New Year’s resolutions that you made but failed to keep. Maybe you decided that you should lose some weight but then never put a concrete plan in action. Maybe you decided that you would read more but didn’t. Why did your goal fail?

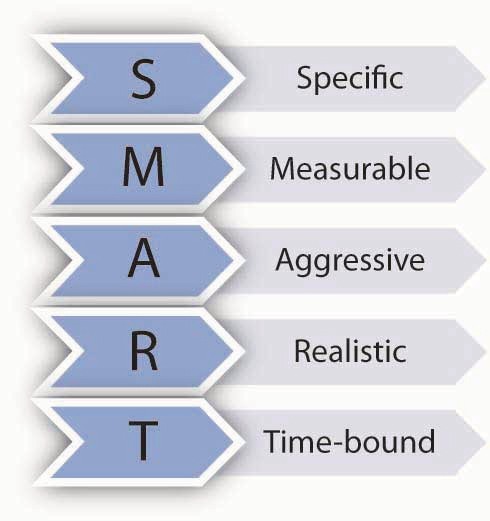

Accumulating research evidence indicates that effective goals are SMART. A SMART goal is a goal that is specific, measurable, aggressive, realistic, and time-bound.

Specific and Measurable

Effective goals are specific and measurable. For example, “increasing sales to a region by 10%” is a specific goal, whereas deciding to “delight customers” is not specific or measurable. When goals are specific, performance tends to be higher (Tubbs, 1986). Why? If goals are not specific and measurable, how would you know whether you have reached the goal? A wide distribution of performance levels could potentially be acceptable. For the same reason, “doing your best” is not an effective goal, because it is not measurable and does not give you a specific target.

Certain aspects of performance are easier to quantify. For example, it is relatively easy to set specific goals for productivity, sales, number of defects, or turnover rates. However, not everything that is easy to measure should be measured. Moreover, some of the most important elements of someone’s performance may not be easily quantifiable (such as employee or customer satisfaction). So how do you set specific and measurable goals for these soft targets? Even though some effort will be involved, metrics such as satisfaction can and should be quantified. For example, you could design a survey for employees and customers to track satisfaction ratings from year to year.

Aggressive

This may sound counterintuitive, but effective goals are difficult, not easy. Aggressive goals are also called stretch goals. According to a Hay Group study, one factor that distinguishes companies that are ranked as “Most Admired Companies” in Fortune magazine is that they set more difficult goals (Stein, 2000). People with difficult goals outperform those with easier goals (Mento, Steel, & Karren, 1987; Phillips & Gully, 1997; Tubbs, 1986; Yukl & Latham, 1978). Why? Easy goals do not provide a challenge. When goals are aggressive and require people to work harder or smarter, performance tends to be dramatically higher. Research shows that people who have a high level of self-efficacy and people who have a high need for achievement tend to set more difficult goals for themselves (Phillips & Gully, 1997).

Realistic

While goals should be difficult, they should also be based in reality. In other words, if a goal is viewed as impossible to reach, it will not have any motivational value. In fact, setting impossible goals and then punishing people for not reaching these goals is cruel and will demotivate employees.

Time-Bound

The goal should contain a statement regarding when the proposed performance level will be reached. For example, “increasing sales to a region by 10%” is not a time-bound goal, because there is no time limit. Adding a limiter such as “by December of the current fiscal year” gives employees a sense of time urgency.

Here is a sample SMART goal: Wal-Mart Stores Inc recently set a goal to eliminate 25% of the solid waste from U.S. stores by the year 2009. This goal meets all the conditions of being SMART (as long as 25% is a difficult yet realistic goal) (Heath & Heath, 2008). Even though it seems like a simple concept, in reality many goals that are set within organizations may not be SMART. For example, Microsoft recently conducted an audit of its goal setting and performance review system and found that only about 40% of the goals were specific and measurable (Shaw, 2004).

Ensuring Goal Alignment Through Management by Objectives (MBO)

Goals direct employee attention toward a common end. Therefore, it is crucial for individual goals to support team goals and team goals to support company goals. A systematic approach to ensure that individual and organizational goals are aligned is Management by Objectives (MBO). First suggested by Peter Drucker (Greenwood, 1981; Muczyk & Reimann, 1989; Reif & Bassford, 1975), MBO involves the following process:

- Setting company-wide goals derived from corporate strategy

- Determining team- and department-level goals

- Collaboratively setting individual-level goals that are aligned with corporate strategy

- Developing an action plan

- Periodically reviewing performance and revising goals

A review of the literature shows that 68 out of the 70 studies conducted on this topic displayed performance gains as a result of MBO implementation (Rodgers & Hunter, 1991). It also seems that top management commitment to the process is the key to successful implementation of MBO programs (Rodgers, Hunter, & Rogers, 1993). Even though formal MBO programs have fallen out of favor since the 1980s, the idea of linking employee goals to corporate-wide goals is a powerful idea that benefits organizations.

Key Takeaways

Goal-setting theory is one of the most influential theories of motivation. In order to motivate employees, goals should be SMART (specific, measurable, aggressive, realistic, and time-bound). SMART goals motivate employees because they energize behaviour, give it direction, provide a challenge, force employees to think outside the box, and devise new and novel methods of performing. Goals are more effective in motivating employees when employees receive feedback on their accomplishments, have the ability to perform, and are committed to goals. Poorly derived goals have the downsides of hampering learning, preventing adaptability, causing a single-minded pursuit of goals at the exclusion of other activities, and encouraging unethical behaviour. Companies tie individual goals to company goals using management by objectives.

Exercises

- Give an example of a SMART goal.

- If a manager tells you to “sell as much as you can,” is this goal likely to be effective? Why or why not?

- How would you ensure that employees are committed to the goals set for them?

- A company is interested in increasing customer loyalty. Using the MBO approach, what would be the department- and individual-level goals supporting this organisation-wide goal?

- Discuss an experience you have had with goals. Explain how goal setting affected motivation and performance.

Motivating Employees Through Performance Incentives

Performance Incentives

Perhaps the most tangible way in which companies put motivation theories into action is by instituting incentive systems. Incentives are reward systems that tie pay to performance. There are many incentives used by companies, some tying pay to individual performance and some to company-wide performance. Pay-for-performance plans are very common among organizations. For example, according to one estimate, 80% of all American companies have merit pay, and the majority of Fortune 1000 companies use incentives (Luthans & Stajkovic, 1999). Using incentives to increase performance is a very old idea. For example, Napoleon promised 12,000 francs to whoever found a way to preserve food for the army. The winner of the prize was Nicolas Appert, who developed a method of canning food (Vision quest, 2008). Research shows that companies using pay-for-performance systems actually achieve higher productivity, profits, and customer service. These systems are more effective than praise or recognition in increasing retention of higher performing employees by creating higher levels of commitment to the company (Cadsby, Song, & Tapon, 2007; Peterson & Luthans, 2006; Salamin & Hom, 2005). Moreover, employees report higher levels of pay satisfaction under pay-for-performance systems (Heneman, Greenberger, & Strasser, 1988).

At the same time, many downsides of incentives exist. For example, it has been argued that incentives may create a risk-averse environment that diminishes creativity. This may happen if employees are rewarded for doing things in a certain way, and taking risks may negatively affect their paycheck. Moreover, research shows that incentives tend to focus employee energy to goal-directed efforts, and behaviours such as helping team members or being a good citizen of the company may be neglected (Breen, 2004; Deckop, Mengel, & Cirka, 1999; Wright et al., 1993). Despite their limitations, financial incentives may be considered powerful motivators if they are used properly and if they are aligned with company-wide objectives. The most frequently used incentives are listed as follows.

Piece Rate Systems

Under piece rate incentives, employees are paid on the basis of individual output they produce. For example, a manufacturer may pay employees based on the number of purses sewn or number of doors installed in a day. In the agricultural sector, fruit pickers are often paid based on the amount of fruit they pick. These systems are suitable when employee output is easily observable or quantifiable and when output is directly correlated with employee effort. Piece rate systems are also used in white-collar jobs such as check-proofing in banks. These plans may encourage employees to work very fast, but may also increase the number of errors made. Therefore, rewarding employee performance minus errors might be more effective. Today, increases in employee monitoring technology are making it possible to correctly measure and observe individual output.

Individual Bonuses

Bonuses are one-time rewards that follow specific accomplishments of employees. For example, an employee who reaches the quarterly goals set for her may be rewarded with a lump sum bonus. Employee motivation resulting from a bonus is generally related to the degree of advanced knowledge regarding bonus specifics.

Merit Pay

In contrast to bonuses, merit pay involves giving employees a permanent pay raise based on past performance. Often the company’s performance appraisal system is used to determine performance levels and the employees are awarded a raise, such as a 2% increase in pay. One potential problem with merit pay is that employees come to expect pay increases. In companies that give annual merit raises without a different raise for increases in cost of living, merit pay ends up serving as a cost-of-living adjustment and creates a sense of entitlement on the part of employees, with even low performers expecting them. Thus, making merit pay more effective depends on making it truly dependent on performance and designing a relatively objective appraisal system.

Sales Commissions

In many companies, the paycheck of sales employees is a combination of a base salary and commissions. Sales commissions involve rewarding sales employees with a percentage of sales volume or profits generated. Sales commissions should be designed carefully to be consistent with company objectives. For example, employees who are heavily rewarded with commissions may neglect customers who have a low probability of making a quick purchase. If only sales volume (as opposed to profitability) is rewarded, employees may start discounting merchandise too heavily, or start neglecting existing customers who require a lot of attention (Sales incentive plans, 2006). Therefore, the blend of straight salary and commissions needs to be managed carefully.

Awards

Some companies manage to create effective incentive systems on a small budget while downplaying the importance of large bonuses. It is possible to motivate employees through awards, plaques, or other symbolic methods of recognition to the degree these methods convey sincere appreciation for employee contributions. For example, Yum! Brands Inc, the parent company of brands such as KFC and Pizza Hut, recognizes employees who go above and beyond job expectations through creative awards such as the seat belt award (a seat belt on a plaque), symbolizing the roller-coaster-like, fast-moving nature of the industry. Other awards include things such as a plush toy shaped like a jalapeño pepper.

Team Bonuses

In situations in which employees should cooperate with each other and isolating employee performance is more difficult, companies are increasingly resorting to tying employee pay to team performance.

Gainsharing

Gainsharing is a company-wide program in which employees are rewarded for performance gains compared to past performance. These gains may take the form of reducing labor costs compared to estimates or reducing overall costs compared to past years’ figures. These improvements are achieved through employee suggestions and participation in management through employee committees.

Profit Sharing

Profit sharing programs involve sharing a percentage of company profits with all employees. These programs are company-wide incentives and are not very effective in tying employee pay to individual effort, because each employee will have a limited role in influencing company profitability. At the same time, these programs may be more effective in creating loyalty and commitment to the company by recognizing all employees for their contributions throughout the year.

Stock Options

A stock option gives an employee the right, but not the obligation, to purchase company stocks at a predetermined price. For example, a company would commit to sell company stock to employees or managers 2 years in the future at $30 per share. If the company’s actual stock price in 2 years is $60, employees would make a profit by exercising their options at $30 and then selling them in the stock market. The purpose of stock options is to align company and employee interests by making employees owners. However, options are not very useful for this purpose, because employees tend to sell the stock instead of holding onto it. In the past, options were given to a wide variety of employees, including CEOs, high performers, and in some companies all employees. For example, Starbucks Corporation was among companies that offered stock to a large number of associates. Options remain popular in start-up companies that find it difficult to offer competitive salaries to employees. In fact, many employees in high-tech companies such as Microsoft and Cisco Systems Inc became millionaires by cashing in stock options after these companies went public. In recent years, stock option use has declined. One reason for this is the changes in options accounting.

Exercises

- Have you ever been rewarded under any of the incentive systems described in this chapter? What was your experience with them?

- What are the advantages and disadvantages of bonuses compared to merit pay? Which one would you use if you were a manager at a company?

- What are the advantages of using awards as opposed to cash as an incentive? How effective are stock options in motivating employees? Why do companies offer them?

- Which of the incentive systems in this section do the best job of tying pay to individual performance? Which ones do the worst job?

Key Takeaways

Companies use a wide variety of incentives to reward performance. This is consistent with motivation theories showing that rewarded behaviour is repeated. Piece rate, individual bonuses, merit pay, and sales commissions tie pay to individual performance. Team bonuses are at the department level, whereas gainsharing, profit sharing, and stock options tie pay to company performance. While these systems may be effective, people tend to demonstrate behaviour that is being rewarded and may neglect other elements of their performance. Therefore, reward systems should be designed carefully and should be tied to a company’s strategic objectives.

Motivating Neurodiverse Individuals

To encourage sustainable growth, many bet performing companies are looking to identify new talent and have found that neurodiverse individuals — those with autism, Asperger’s syndrome, dyslexia, attention deficit hyperactivity disorder, and dyspraxia — can create innovation and contribute to the skills needed for emerging areas such as artificial intelligence, automation, blockchain, cybersecurity and data management (Twaronite, 2020). Over 15% of the Canadian workforce is neurodiverse, and leveraging the unique capabilities of these employees is becoming a competitive advantage among organizations (Bitti, 2022). Some researchers claim that “Neurodiversity is a moral, social, and economic imperative; everybody loses when human potential is squandered” (Doyle, 2021, p. 194). Leveraging the unique talents of neurodiverse individuals involves having an environment that inspires and motivates them. In a seminal article by Szulc, Davies, Tomczak, & McGregor (2021) researched how best to motivate neurodiverse individuals in a remote workplace environment. They make several recommendations drawing on the ability, motivation, and opportunity (AMO) model and an emerging strength-based approach to neurodiversity. Her recommendations are summarized below:

Szulc, Davies, Tomczak, & McGregor (2021) concluded that in order best to leverage the skills and capabilities of not only neurodiverse individuals but all individuals working remotely while enhancing their motivation, organizations should:

- Offer flexible hours of work

- Set up support groups as platforms for questions and feedback and as a place to share strategies for remote work.

- Ask proactively about accommodations needed.

- Introduce and support mentoring and coaching (e.g., team buddies, job coaches)

Conclusion

In this chapter, we reviewed specific methods with which companies attempt to motivate their workforce. Designing jobs to increase their motivating potential; to empower employees; to set goals; to evaluate performance; to offer performance appraisals; and tying employee pay to individual, group, or organizational performance using incentive systems are methods through which motivation theories are put into action. Even though these methods seem to have advantages, every method could have unintended consequences, and therefore, application of each method should be planned and executed with an eye for organizational fairness.

Individual Exercise

A call center is using the metric of average time per call when rewarding employees. In order to keep their average time low, employees are hanging up on customers when they think that the call will take too long to answer. In a department store, salespeople are rewarded based on their sales volume. The problem is that they are giving substantial discounts and pressuring customers to make unnecessary purchases. All employees at a factory are receiving a large bonus if there are no reported injuries for 6 months. As a result, some employees are hiding their injuries so that they do not cause others to lose their bonus. What are the reasons for the negative consequences of these bonus schemes? Modify these schemes to solve the problems.